EIB #18 - "You're Hired!" Picking Powell's Successor

Jobs smash expectations, "no recession" in May and June, ideas for picking Powell's successor, and Powell's "Marbury moment" to secure the Fed's independence.

All,

In today’s EIB, please find:

Key Takeaways from Today’s Jobs Report

The U.S. economy added 147k non-farm jobs, beating expectations of 110k.

The headline unemployment rate was 4.1%, little changed from last month.

Tentative “no recession” calls for May and June 2025

Feel free to forward or subscribe. (It’s free.) Have a happy Independence Day!

Best,

Chris

Fact of the Week: Federal net interest expenses now average $3.3 billion per day.

Key Takeaways from Today’s Jobs Report

At 8:30am ET, the BLS announced that in June:

The U.S. economy added 147k non-farm jobs, beating expectations of 110k.

74k jobs were added in the private sector, almost all in services.

Notable gains in state government (47k) and health care (39k).

Federal employment fell by 7k and is down 69k since January.1

The headline unemployment rate was 4.1%, little changed from last month.

The BLS revised up its jobs estimates for March and April by a combined 16k.

Wages likely kept pace with consumer prices. Average hourly earnings rose by 8 cents (0.22% m/m). The Cleveland Fed nowcast that the CPI rose by 0.25% m/m.

Messaging

This is a good report for messaging. Jobs added soundly beat expectations, wages are growing faster than prices, federal employment continues to fall without catastrophe.

Yesterday, the stock market hit an all-time high (as measured by the S&P 500 index). Stock futures are trading up this morning. The 10-year yield is trading around 4.3%.

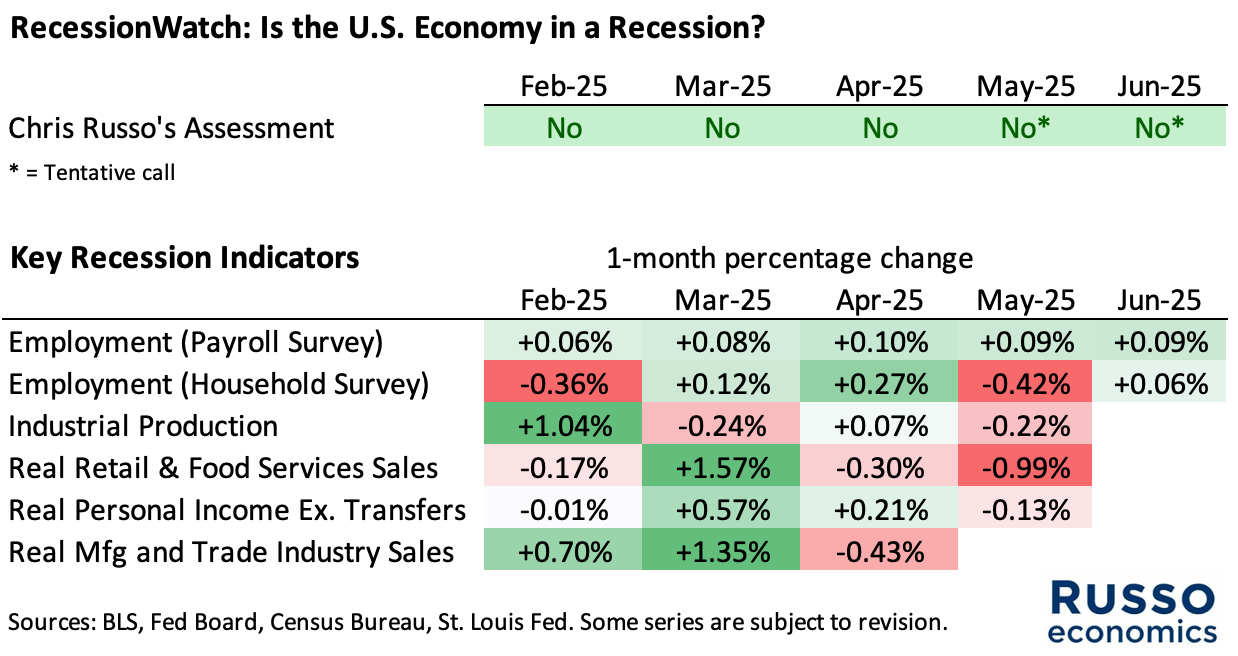

RecessionWatch

BLUF: I confirm my “no recession” call for April 2025. I make a tentative “no recession” call for May 2025, despite a string of bad data prints. I make a tentative “no recession call” for June 2025 on the strength of this morning’s jobs numbers.2

In my last RecessionWatch update, I postponed making a recession call for May. I was spooked by the contraction in employment reported by the Household Survey, as well as by the large downward revisions to employment reported by the Payrolls Survey.

My hesitation was warranted: June was filled with bad news for the U.S. economy.

Four of five “key recession indicators” were negative in May. Of note:

Jobs added (household survey) was worse than 96% of months since 1948.

Real Retail & Food Service Sales was worse than 90% of months since 1992.

The Atlanta Fed’s GDPNow estimate for Q2 was revised from 4.7% to 2.5%.

The Atlanta Fed model tracks a wider variety of incoming economic data.

The downward revision indicates that data were much weaker than expected.

That said, one bad month does not make a recession. Moreover, the declines for two key recession indicators (IP and RPIxT) were quite modest. Even during economic expansions, we should expect occasional declines due to monthly volatility. In my judgment, these declines were not so large as to indicate we are headed into recession.

In June, the string of downwards jobs revisions was ended, and employment (as measured by the household survey) did not continue to fall. Other labor market indicators (e.g., the unemployment rate and UI claims) remain around healthy levels. Alternative indicators are mixed, but indicate to me that consumer demand is healthy.

Picking the Next Chairman of the Federal Reserve Board

The media is already buzzing about who will replace Jay Powell, whose term as Fed chairman expires on May 15, 2026. Some names tossed around include, inter alia, former Fed governor Kevin Warsh, NEC director Kevin Hassett, Treasury secretary Bessent, Fed governor Chris Waller, and former World Bank president David Malpass.

Pres. Trump will announce his pick this fall, or maybe sooner. By announcing the pick early and loudly, Pres. Trump seemingly wants to make Powell a lame duck. If that is his strategy, then here is what Pres. Trump should do to maximize media coverage.

Pres. Trump should host an Apprentice-style show to pick the next Fed Chairman. Make it a one-hour or two-hour special on prime time TV. Some ideas:

Contestants debate monetary policy in a format moderated by Pres. Trump.

Contestants are split into two teams and redesign the U.S. dollar bill.

Contestants create a viral social media campaign to improve the Fed’s PR.

We would also need some celebrity judges. What’s Dennis Rodman up to these days? Or Rod Blagojevich? For the younger audience, how about a collab with Mr. Beast?3

In the final boardroom scene, Pres. Trump evaluates the contestants based on their performance, personality, and their willingness to cut interest rates by at least 2.5%.

Chairman Powell’s Marbury Moment

Among academics, Marbury v. Madison is a famous case for more than its application of judicial review. In Marbury, chief justice John Marshall faced a politically fraught dilemma. At stake in the case was the fledgling court’s power and credibility.

If Marshall ruled in favor of Marbury and required Madison to deliver his commission, then Madison may have just ignored the ruling. Without a way to enforce its ruling, the Supreme Court would have looked utterly impotent.

If Marshall ruled against Marbury and did not require Madison to deliver his commission, then Marshall (a Federalist) would have handed Jefferson (a Democratic-Republican, and Marshall’s arch rival) a major political victory.

Marshall devised the following ruling that cemented the Supreme Court’s power and credibility, while giving Jefferson a small victory he could not defy or protest. Namely:

Withholding Marbury’s commission was illegal. Marbury had a legal right to it.

However, the Court did not have jurisdiction over the case because the act that purported to give the it jurisdiction violated Article III of the Constitution.

Therefore, the Court could not order the administration to award the commission.

Notice the two-step. By accepting a limit on the court’s power (jurisdiction), Marshall cemented the court’s power of judicial review. Moreover, by giving Jefferson a limited victory, he disarmed the threat of noncompliance with the court. Despite Jefferson’s hatred of judicial review, he could not reasonably contest a ruling in his own favor.

I believe Chairman Powell has an opportunity for his own Marbury moment. As Pres. Trump searches for his nominee, it is no secret that the chief job requirement is a willingness to slash interest rates. Cutting rates may even be the right policy! However, such a demand on the Fed chairman threatens the Fed’s independence.

That limited independence is key to the Fed’s ability to control inflation. It means that the Fed can set interest rates based on economic conditions, not politics. Ironically, while Pres. Trump’s stated goal is to reduce federal interest expense, it is the Fed’s control of inflation since the 1990’s that has helped lower long-term rates.4

OK, here is how Powell can secure the Fed’s independence by accepting a limit on his power and giving Pres. Trump a limited victory: adopt a rules-based monetary policy.

From EIB #16, recall that a simple monetary policy rule (a/k/a Taylor rule) has the form:

Remember, the left-hand side is the prescribed interest rate. The right-hand side are variables that the Fed either picks, observes, or estimates from other economic data.

To keep it simple, suppose the Fed does not worry about the output gap (β = 0), the Fed reacts 1.5-to-1 to deviations of inflation from target (α = 1.5), the inflation target is unchanged at 2% (π* = 2%), and the Fed estimates a natural rate of 1% (r* = 1%).5

While the Fed could do something more complicated, this results in an ultra simple monetary policy rule: the Fed sets overnight rates at 1.5 times the inflation rate.

And because Chairman Powell has regularly emphasized being “data dependent,” the FOMC can just plug in the current 12-month PCE inflation rate into this formula.6 Since the current PCE inflation rate is 2.34%, this prescribes an interest rate of 3.51%.

Upon announcing and adopting such a rule, the Fed would immediately cut by 0.8%.7 This would give Pres. Trump a political win: “too late” Jay Powell finally agrees that Pres. Trump was correct about rate cuts, and the size of the cuts is unprecedented outside of recessions. Pres. Trump could not protest or defy this political victory.

At the same time, by adopting a rules-based monetary policy, the Fed would secure its own operational independence. Since monetary policy decisions are made by rule (and not by discretion), the identity of the next chairman is irrelevant to the stance of monetary policy. The President cannot put political pressure on a mathematical rule.

Upcoming Data Releases

July 15, 8:30am ET. The BLS releases the CPI report for June. The Cleveland Fed nowcast is 0.25% m/m (2.64% y/y), implying that inflation is still above target.

July 30, 8:30am ET. The BEA releases its “advance” estimate of real GDP for Q2. The Atlanta Fed’s GDPNow model estimates real GDP growth is 2.5% (SAAR).

July 30, 2:00pm ET. Federal Reserve announces monetary policy decision. The current target range for overnight interest rates is 4.25% to 4.50%. Owing to solid job growth, above target inflation, and heightened economic uncertainty, options markets are pricing an 93% chance the Fed will keep the target range unchanged.

Employees on paid leave or receiving ongoing severance are counted as “employed” in the payroll survey.

RecessionWatch provides real-time analysis of whether the U.S. economy is in a recession. Whereas the NBER usually takes between 4 and 21 months to “officially” call a recession, I make tentative recession calls at the start of each month. RecessionWatch is not a recession forecast. I am not predicting whether there will be a recession (e.g.) next month or next year.

This single name exhausts my knowledge of Gen Z and Gen Alpha celebrities/influencers.

Lenders require higher interest rates to compensate for expected inflation. Think about it this way. Suppose you’ve taken out a mortgage at a 3% interest rate. The bank priced this loan expecting a 2% inflation rate, so the ex ante “real” (i.e., inflation adjusted) interest rate is 1%. But actually, inflation rises to 3% and stays there for the life of the mortgage. The ex post real interest rate is 0%. You’re paying 3% per year, but the loan balance you owe is worth 3% less. To compensate for higher inflation, the bank hikes the mortgage rate to 4%.

If the Fed can control inflation and thereby bring down inflation expectations, then long-term rates will fall.

Assuming 2% expected inflation, a natural real rate of interest of 1% is consistent with the median projection for the longer-run fed funds rate of 3% from the June 2025 SEP.

PCE inflation is the Fed’s preferred measure, and tends to run a bit cooler than CPI inflation. Again, this choice works in the President’s favor: lower inflation = lower rates.

The current EFFR is 4.33%. Therefore, a prescribed EFFR of 3.51% implies a roughly 0.8% cut. This is roughly three “standard” sized cuts of 0.25%.